Loading...

February 9, 2026

ATO Business Tax Updates 2025: What Every Business Owner Must Know

Lodge Pro•Blog•5 min read

Check your PAYG instalments

Now is a good time to check that your business’ PAYG instalments still reflect the expected end-of-year tax liability.

If your business’ circumstances have changed and you think you will pay too much (or too little) in instalments for the year, the instalments can be varied on the next activity statement (due on 28 April 2024 if you pay quarterly). Instalments can be varied multiple times throughout the year. The varied amount or rate will apply for the remaining instalments for the income year or until another variation is made.

If your varied instalments are less than 85% of your total tax payable, you may have to pay a general interest charge on the difference, in addition to paying the shortfall. Depending on the circumstances there may also be penalties.

If you are not sure, it is best to not vary your instalments. Any overpaid instalments will be refunded to you after you lodge your tax return.

If your business is affected by COVID-19 or a natural disaster, the ATO has said it will not apply penalties or charge interest to varied instalments if you have made your best attempt to estimate your end of year tax liability.

If an amount or rate is varied online, activity statements and instalment notices will be issued electronically and not in paper form. You will need to consider this when deciding how to lodge, revise and vary future activity statements and instalment amounts.

Tip!

Your tax adviser or BAS agent can help you with your activity statements and tax returns.

Can you claim the small business skills and training boost?

If you are paying for your employees’ external training, you could be eligible to claim the skills and training boost.

Businesses with an aggregated annual turnover of less than $50 million are potentially eligible for the small business skills and training boost. The boost provides an additional 20% bonus tax deduction for eligible expenditure incurred on training new and existing employees.

If eligible, you can claim a deduction on expenditure for external training courses delivered to your employees, either in person in Australia or online. The training must be provided by a registered external training provider.

The skills and training boost is available until 30 June 2024, so you still have time.

You cannot claim expenditure for training you undertake yourself as a business owner, such as where you are a sole trader, partner in a partnership or independent contractor.

Example

If you are a gardener operating as a sole trader, and you and your employee begin turf management training, you cannot claim the bonus deduction for the expenditure on training for yourself, but you can claim it for your employee’s training.

Tip!

Talk to your tax adviser to see if you are eligible for the skills and training boost.

Starting a franchise

With franchising, the franchisor grants a right to the franchisee to:

use a business brand name or trademark; and

produce or distribute their product or service

The franchisor and each franchisee have their own Australian Business Number (ABN).

The franchisee incurs franchise-specific payments made to their franchisor in addition to other general business expenses. Some of these payments are deductible and others are capital in nature and not deductible.

Common franchise fees

Common franchise fees are:

Franchise establishment fees — the franchise establishment fee or transfer fee forms part of the cost base for your franchise licence, which is a capital asset. Because these fees are a capital investment in your business, they are not tax deductible.

Franchise renewal fees — if your franchise renewal fees form part of your cost base, they will not be deductible. Any franchise renewal fees not included in your cost base may be deductible as a business expense and are subject to the prepayment rules.

An example of where you would not include a franchise renewal fee in your cost base is where it is for a relatively short period (for example, 5 years), and you would be left with no franchise if you did not pay the renewal fee.

Royalties, interest and other payments to the franchisor

An agreement to buy a franchise often includes ongoing royalty payments, interest payments or levies to the franchisor. These payments typically cover head office expenses, such as administration, advertising and technical support.

Royalty payments, interest payments and levies to the franchisor can be claimed as an expense on your annual tax return. This is because they are an ongoing expense in running your business.

Royalty and interest payments to non-residents

Generally, when you make royalty and interest payments to non-resident franchisors, you are required to withhold a flat rate of:

30% from the gross amount of a royalty payment; and

10% from the gross amount of an interest payment.

However, where there is a tax treaty agreement with the non-resident’s country of residence, you apply the withholding rate in the tax treaty.

You pay and report the amounts you withhold from interest and royalty payments in your business activity statement (BAS) for the relevant reporting period.

You report the total annual amount of royalty and interest payments, and amounts withheld, in the PAYG withholding from interest, dividend and royalty payments paid to non-residents – annual report.

If you are required to withhold tax from a royalty or interest payment to a non-resident, you can claim a deduction for it only if:

you have withheld tax from the payment and paid the withheld amount to the ATO; or

the withholding tax is paid.

Training fees

You can claim a tax deduction for fees you pay to the franchisor for ongoing training for employees in their roles.

GST

If the franchisor is registered for goods and services tax (GST), payments you make to the franchisor may include a GST component.

If you are registered for GST, you may be able to claim a GST credit in your BAS for the GST amount included in:

the initial franchise fee.

franchise renewal fees.

franchise service fees or royalties.

advertising fees.

transfer fees.

training fees.

Transferring or terminating a franchise

If you transfer a franchise to another party or end your franchise agreement, there may be capital gains tax (CGT) and GST consequences.

When you transfer or end your franchise agreement, you will need to calculate your CGT and include that in your annual tax return.

The sale of an existing franchise by a franchisee may qualify as a GST-free sale of a going concern.

Tip!

If your business is considering starting a franchise, or if you are already a franchisee and you are thinking about selling the franchise, contact your tax adviser to discuss all the tax implications.

EV home charging rates

The ATO allows a cents-per-kilometre methodology for calculating electricity costs where an electric vehicle (EV) is charged at an employee’s home.

The employer can choose to use this methodology instead of determining the actual cost of the electricity. The choice is per vehicle and applies for the whole income or FBT year. However, it can change from year to year.

The methodology does not apply to plug-in hybrid vehicles, electric motorcycles or electric scooters.

Cents-per-kilometre

The ‘EV home charging rate’ is 4.2 cents per km. This rate is multiplied by the total number of relevant kilometres travelled by the EV in the income year or FBT year in question.

Where EV charging costs are also incurred at commercial charging stations and the home charging percentage can be accurately determined, the total number of relevant kilometres must be adjusted. If the home charging percentage cannot be accurately determined, you can choose to use either the EV home charging rate and disregard the commercial charging station cost, or the commercial charging station cost and not apply the EV home charging methodology.

Record keeping and transitional approach for 2022–23 and 2023–24

If you are an employer and you choose to apply the EV home charging rate for FBT purposes, a valid logbook must be maintained if the operating cost method is used.

To satisfy the record keeping requirements for income tax purposes:

a valid logbook is needed to use the logbook method of calculating work-related car expenses. For other vehicles, the ATO recommends a logbook to demonstrate work-related use of the vehicle; and

one electricity bill for the residential premises in the income year is needed (to show that electricity costs have been incurred).

However, if you have not maintained odometer records as at the start of the 2022–23 or 2023–24 FBT or income year, the ATO will allow a reasonable estimate to be used based on service records, logbooks or other available information.

How to nail your record keeping

Good record keeping helps you manage your business and cash flow, and ensures you get the right outcome with your business’ tax return.

The following tips can help you get it right. They are based on common record keeping errors seen by the ATO.

Keep accurate records of all cash and electronic transactions.

Reconcile cash and EFTPOS sales regularly and enter the amounts into your accounting software.

Check for mistakes if things do not add up.

Accurately record the business portion of mixed-use expenses.

Account for trading stock used privately.

Ensure you have sufficient records to substantiate business expenses claimed as tax deductions.

Do not use estimates when preparing tax returns or BAS.

Keep most records for 5 years, or longer where required.

Retain records for tax losses and capital losses until fully applied.

Keep detailed contractor records for TPAR reporting.

Separate GST records where claiming GST credits.

Retain PAYG payment summaries where amounts were withheld.

Digital record keeping

There are advantages to keeping business records digitally, including:

tracking income, expenses and assets;

streamlining accounting practices;

calculating wages, tax and super;

meeting STP obligations;

backing up records securely in the cloud.

If your business uses cloud storage, ensure:

the storage meets record keeping requirements;

you download a complete copy before changing providers.

eInvoicing storage

Regardless of your business’ eInvoicing software or system, you are responsible for determining the best option for storing business transaction data.

You should:

ensure that the process meets the record keeping requirements;

discuss options with the software provider;

talk to your business adviser if necessary.

Tip!

Not sure what records you should keep and how long you should keep them for? Talk to your tax adviser or BAS agent.

Registered emissions units

A registered emissions unit (REU) is a unit recorded in the Australian National Registry of Emissions Units. There are three types:

a Kyoto unit;

an Australian carbon credit unit (ACCU);

a safeguard mechanism credit unit.

A special tax regime applies to REUs and the normal rules, such as CGT, do not apply.

Basic tax treatment of REUs

Certain acquisition costs are deductible.

Changes in value may be assessable or deductible.

Disposal proceeds are assessable income.

Valuation methods

FIFO cost method

Actual cost method

Market value method

Once chosen, the method must generally be used for at least three years.

Payments in respect of software and IP rights

The ATO has released a revised draft ruling on when payments under software arrangements are royalties.

Payments treated as royalties include:

granting rights to use IP.

using IP.

supplying know-how.

distributing hardware with embedded software using IP rights.

Payments not treated as royalties include:

distribution rights without copyright use.

transferring all rights to software.

hardware sales without IP rights.

Do you use AI?

If your business uses artificial intelligence, new guidance from the Australian Cyber Security Centre can help you manage risks.

Key steps include:

applying the Essential Eight framework.

understanding system limitations.

managing privacy and data protection.

ensuring secure-by-design services.

having qualified staff maintain systems.

FBT issues

FBT return time

The FBT year runs from 1 April to 31 March. The 2023–24 FBT return is due 27 May 2024.

Key points:

All activity statements must be lodged first.

Tax agents extend the due date to 25 June 2024.

First-time agent lodgers must contact their agent by 21 May 2024.

Paying FBT

Shortfalls must be paid.

Excess instalments are refunded.

FBT of $3,000 or more triggers quarterly instalments next year.

What’s new in FBT?

Employee declarations

Make and model details are no longer required in several declarations.

Record keeping changes

From 1 April 2024, alternative records may be used in specified situations if approved by the ATO.

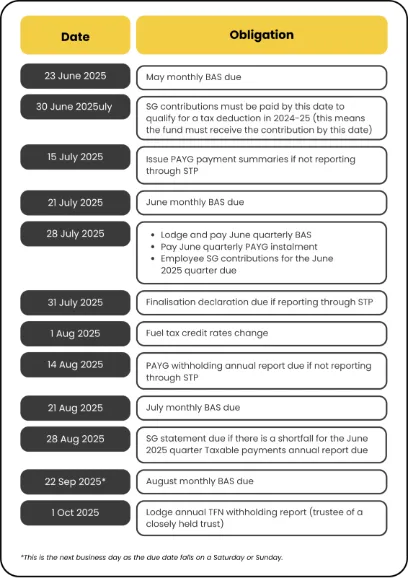

Key tax dates

Next business day where due date falls on a weekend.

Note!

Talk to your tax agent to confirm the correct due dates for your own tax obligations.

DISCLAIMER

TaxWise® News is distributed by professional tax practitioners to provide information of general interest to their clients. The content of this newsletter does not constitute specific advice. Readers are encouraged to consult their tax adviser for advice on specific matters.