Loading...

February 17, 2026

Retirement Planning in Australia: Practical Guide for Your 40s, 50s & 60s in 2026

Lodge Pro•Blog•5 min read

In this article, we will discuss:

Why retirement planning looks different in 2026

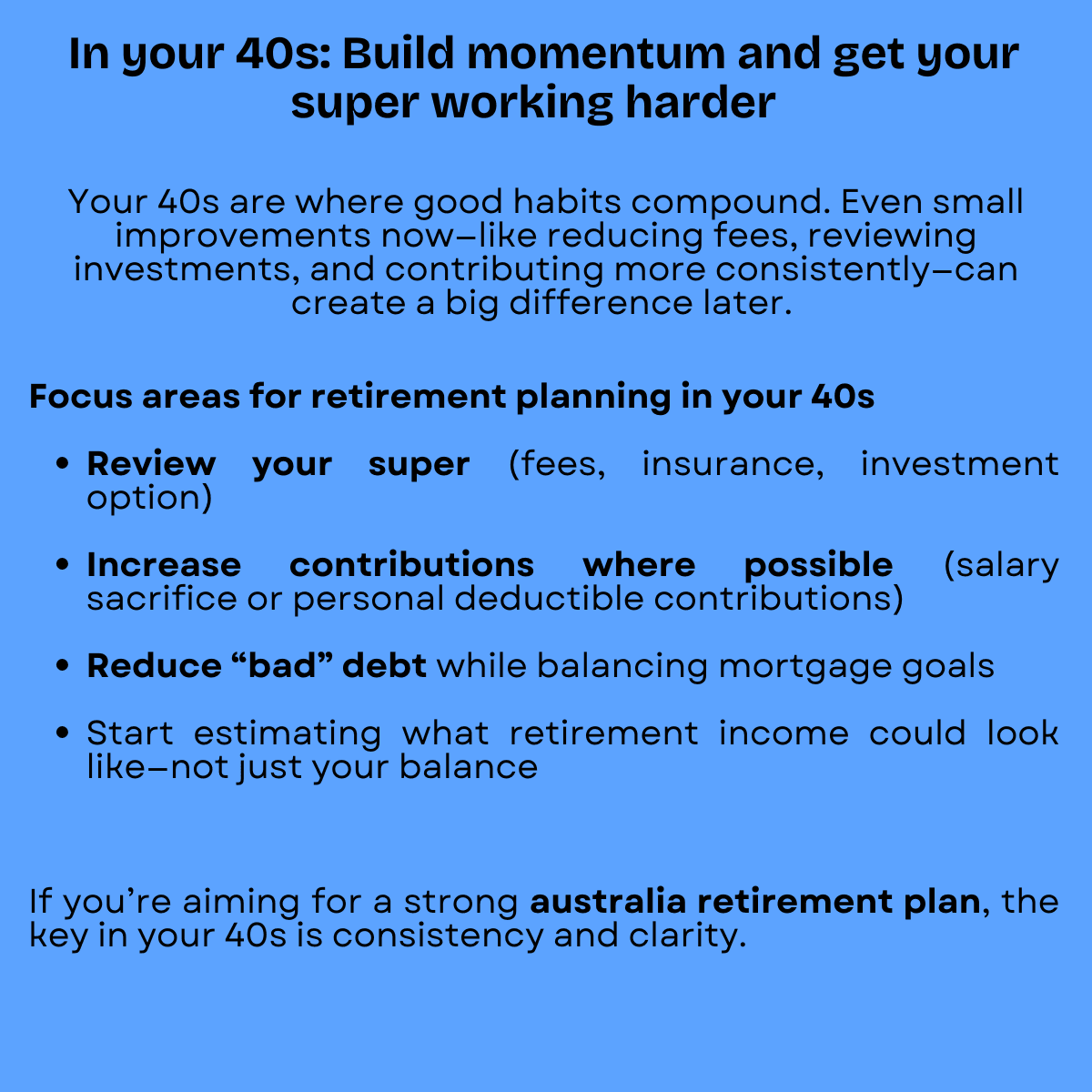

Retirement planning in your 40’s

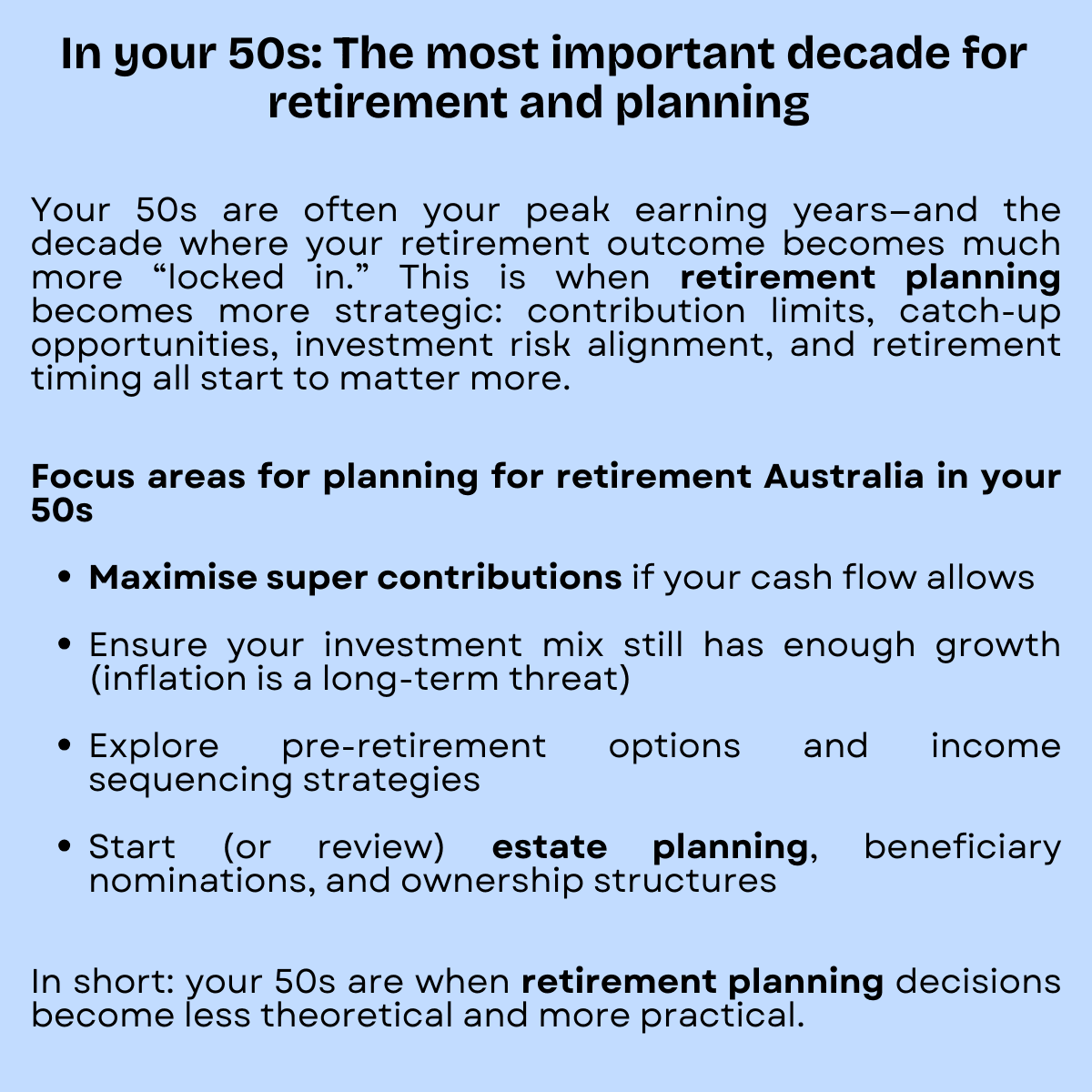

Retirement planning in your 50’s

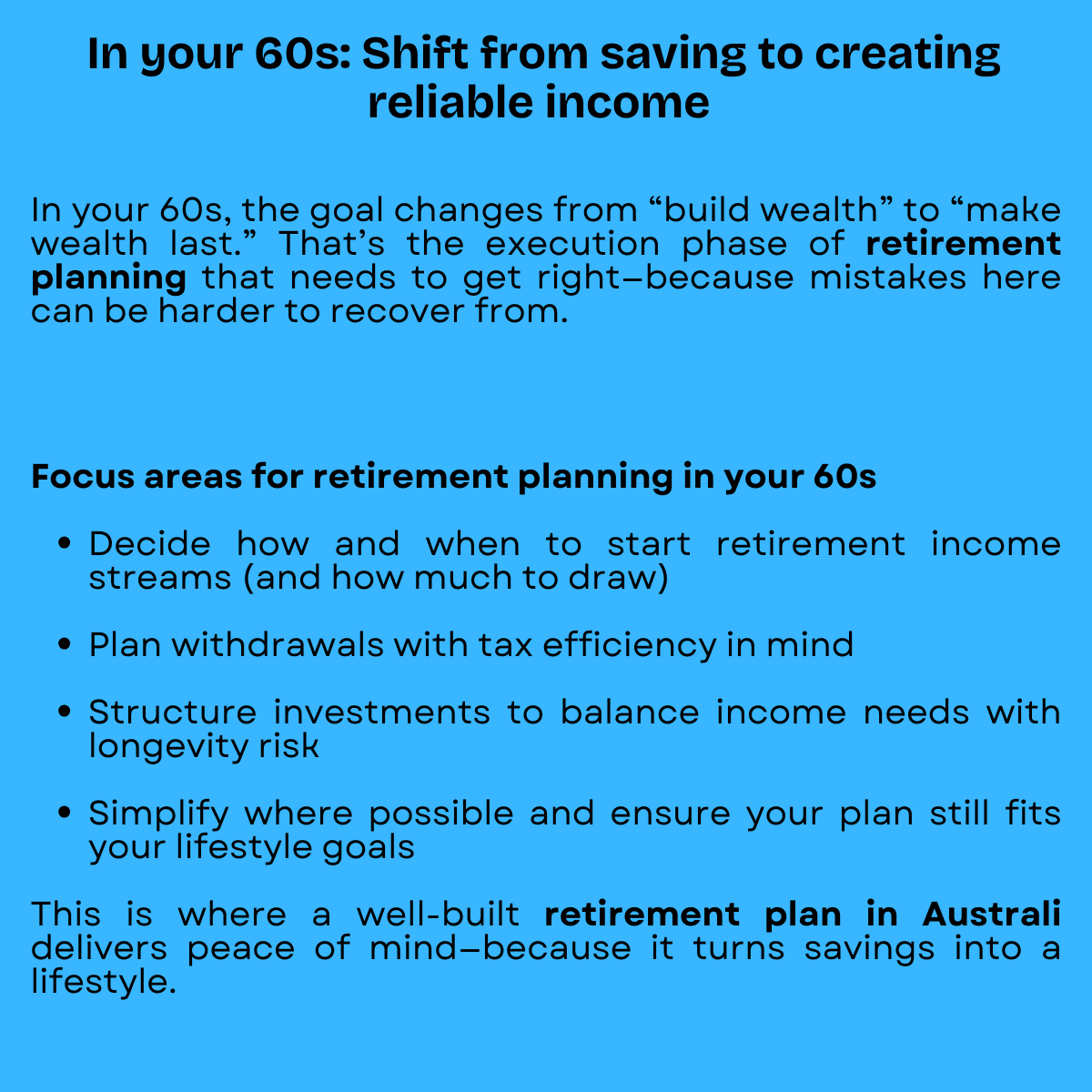

Retirement planning in your 60’s

Common retirement planning mistakes to avoid at any age

Case Study - How Lodge Pro can help

Retirement planning in Australia isn’t a once-off decision—it’s an evolving strategy that should change as your life, income, and priorities change. If you’re serious about planning for retirement in Australia (with super rules, tax considerations, and lifestyle goals in mind), a decade-by-decade approach helps you take the right steps at the right time.

This Australia retirement plan guide breaks down what to focus on in your 40s, 50s, and 60s so you can move from “hoping it works out” to feeling confident about your future.

Why retirement planning in Australia looks different in 2026

In 2026, when planning for retirement in Australia, residents face a mix of opportunity and complexity: changing super contribution rules, inflation pressure, market volatility, and longer life expectancy. That means retirement planning is less about hitting one magic super balance and more about building a sustainable retirement income strategy.

A smarter approach is to think in phases:

Build momentum (40s)

Accelerate and structure (50s)

Execute and protect (60s)

That’s the backbone of effective retirement planning families can actually follow.

Retirement planning in your 40’s

Retirement Planning in your 50’s

Retirement Planning in your 60’s

Common retirement planning mistakes to avoid at any age

No matter your decade, these traps can derail planning for retirement Australia wide:

Delaying decisions because retirement feels “far away”

Focusing only on super balance instead of retirement income

Being too conservative too early (or too aggressive too late)

Not updating estate plans, beneficiaries, or insurance as life changes

How Lodge Pro Helped Sarah Take Control of Her Retirement

When Sarah, 52, first approached Lodge Pro, she felt behind. She had superannuation, a mortgage nearly paid off, and a rough idea of when she wanted to retire — but no clear retirement planning strategy.

She was unsure whether her super was invested correctly, if she was contributing enough, or what her actual retirement income might look like. Like many Australians, she had an account balance… but no real retirement plan.

We at Lodge Pro started by reviewing her super, fees, and investment mix. We identified opportunities to boost her concessional contributions and adjusted her portfolio to better align with her timeline. We also modelled different retirement scenarios so Sarah could see how small changes today would impact her future income.

Within 12 months:

She increased her super contributions tax-effectively

Reduced unnecessary fees

Created a clear roadmap for planning for retirement in Australia

Gained confidence about when she could realistically retire

Today, Sarah doesn’t just have savings — she has structure, clarity, and a personalised retirement and planning strategy designed around her lifestyle goals.

That’s the difference Lodge Pro makes: turning uncertainty into a clear, achievable plan.